Would you rather have £1 million today or a penny (£0.01) that doubles in value every day for 30 days? The answer may surprise you!

If you chose the £1 million today, you’d miss out on over £4.3 million. That’s right! At the end of the month, the penny turns into £5,368,709.

This is the reason Albert Einstein said,

Compound interest is the eighth wonder of the world. He who understands it earns it. He who doesn’t pay it.

So, what is compound interest, and how can you use it to your advantage? Well, you’re in the right place.

What Is Compound Interest?

Compound interest is the interest added to the principal (initial) investment, savings account balance, or loan, as well as all previously accumulated interest. In other words, it’s interest on interest, which helps money grow exponentially over time.

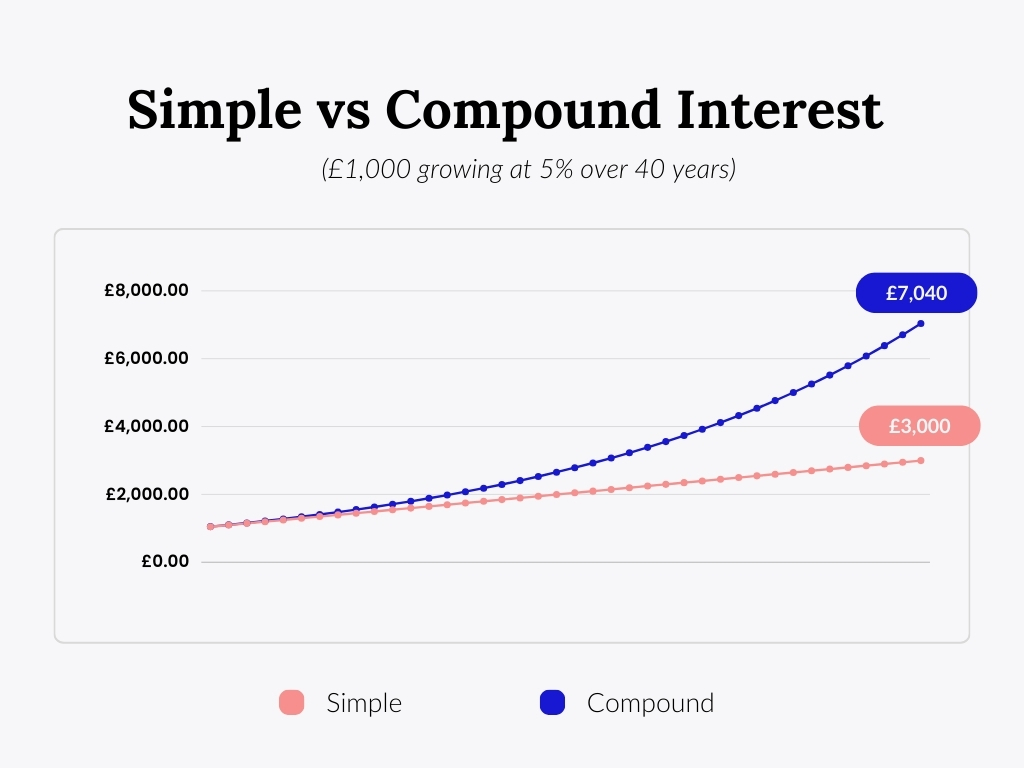

Battle of the Interests: Simple vs Compound

The main difference is that simple interest disregards all previously accumulated interest. So, while your money grows exponentially with compound interest, it grows linearly with simple interest.

Example

Imagine you add £1,000 to a savings account that pays 5% interest.

- With simple interest: After 10 years, you’d have £1,500.

- With compound interest: After 10 years, you’d have £1,629.

The difference may seem small now. But over decades? That’s where compound interest shines.

Compound Interest Formula

The compound interest formula is relatively straightforward. It’s one of the easier formulas in finance, excluding the basic additions, subtractions, multiplications and divisions.

Compound interest formula:

Where:

- A = your final amount

- P = the principal (what you started with)

- r = annual interest rate

- n = the number of times interest compounds per year

- t = time in years

If you plug in the figures from the example above, you should get the £1,629 we calculated. (Our figure is rounded. Unrounded = £1,628.89.)

1,629 = 1,000 * (1 + (5%/1))^(1*10)

The interest in most savings accounts and on investments compounds annually. Therefore, n = 1.

The Magic of ‘t’ – Why Starting Early Matters

Time is the most essential factor in growing your money with compound interest. But why is it so important?

Answer: Its position in the formula.

The compound interest formula is raised by time (t). Therefore, t acts as a multiplier. If you think of it in plain maths, it’s a bit clearer. 2 represents the principal (P), while the changing figures represent time (t).

- 21 = 2

- 22 = 4

- 25 = 32

- 210 = 1,024

The higher ‘t’ gets, or the more time you let compounding work, the greater the multiplier effect and the more wealth you’ll build.

Take, for another example, two 65-year-old investors, Sam and Jack, who invested £100/month at an 8% annual interest rate. Sam started at age 20 and stopped when he turned 30 (he invested £12,000). Jack began at age 30 and stopped when he turned 60 (he invested £36,000).

At 60, Sam ended with £181,342, while Jack grew his money to £140,924. Despite investing three times more than Sam (£36,000 versus £12,000), Jack still fell short by over £40k.

To throw a spanner in the works…if Sam continued investing £100/month until he was 60, he would have grown £48,000 to just over £320,000.

It all boils down to time. Time is your best friend.

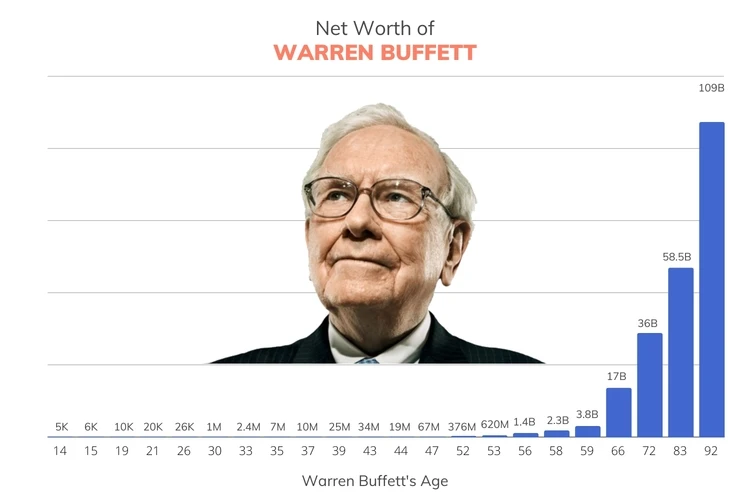

Fun Fact

99% of Warren Buffett’s net worth was earned after his 50th birthday. He is the CEO of Berkshire Hathaway and is worth $163 billion. 99% of that is $161 billion.

For some context, Buffett started investing when he was 11. So, from 11 to 50, his net worth grew to about $2 billion. The rest is just time and compounding.

(Image Source: Finmasters)

Want the breakdown of Buffett’s net worth by age? Click here, then.

3 Ways To Use It To Your Advantage

Now, to the good part – how to benefit from compound interest.

Start As Early As Possible

We alluded to this earlier: time is the most influential factor in compounding. The more time you allow compound interest to work, the more your money grows. Think about Sam and Buffett in the previous section. They gave their money time to compound, and it sure did.

Reinvest Your Earnings

The interest you receive on savings or the dividends from investments can go a long way when compounded. Interest and dividends are rewards for saving and investing, so put them back to work to increase your overall reward.

Minimise Fees & Taxes

While this is especially true for investors and aspiring investors, there are implications for savers. Fees are the silent killers of wealth building, so you want to do everything you can to keep them near zero or zero (if possible).

To minimise fees:

- Ensure your investment account has no hidden charges. The same applies to savings accounts.

- For ETF investors, keep the fund’s expense ratios low.

To minimise taxes (legally):

- Use tax-exempt accounts like ISAs (individual savings accounts) in the UK. ISAs are available to savers and investors, and any gains made in these accounts aren’t taxable by HMRC.

- For investors, keep your selling activity to a minimum. The less you sell, the less capital gains tax you pay.

Debt & Compound Interest

We’ve been talking in glowing terms about compound interest, but you need to know that it also works against you. Compound interest also applies to debt.

Credit Cards

If you carry a balance on your card, interest will compound on the unpaid amount. This is the reason your balance may not decline even though you’re making the minimum monthly payments.

Loans & Mortgages

While longer loan terms may take some of the burden off in the short term, you end up paying more in interest in the long run. This is why you hear people saying they paid for their house twice by the time the mortgage was paid off – it’s the compounded interest.

Student Loans

Same story, different title. Depending on the student loan organisation you use, interest starts to compound from your first day of school. So, what should be the start of a new and exciting journey is often the start of future financial woes for some.

So…How To Avoid The Harmful Effects Of Compound Interest?

The best way? Avoid debt entirely. But if it’s too late for that, then:

- Pay off high-interest debt as quickly as possible.

- Make more than the minimum payments (if possible) to reduce interest accumulation.

- Don’t spend on the credit card – if you’re working to reduce the debt, why increase it?

- Once you become debt-free, steer clear of it, or at least keep it to a minimum.

Common Myths & Misconceptions

As with all things and everything, there are myths, and some myths need debunking. So, here are a few for compound interest.

“You need a lot of money to benefit.”

Small investments and savings contributions add up over time. If you’re consistent enough and let compound interest do its thing, your ‘little’ money can grow into something meaningful.

“It’s only for investors.”

Compound interest isn’t just for stock market investors; it applies to savings accounts, bonds, pensions and debts. Any financial product that earns (or charges) interest benefits (or harms) from compounding.

Ensure you’re on the side that benefits from compounding, not harmed by it.

“Interest rates don’t matter much.”

Said no one ever. Even the slightest differences can have huge impacts over decades.

Investing £100/month for 40 years at 10% gets you to £555,454 – over half a million pounds. At 9.5%, you’d be at £484,020, and 9%, £422,184. A 0.5 percentage point difference and over £70,000 disappears. An entire percentage point and over £133,000 is gone.

Nothing changed except the interest rate.

Rounding It Up!

Compound interest is one of the most influential formulas in all of finance. By understanding how it works and applying it early, you can earn it, as Einstein said.

Key takeaways:

- Compound interest helps money grow exponentially – remember Buffett? And let’s not forget Sam.

- Starting early makes a huge difference – time is your best friend.

- Reinvest your earnings – if you are rewarded for doing something, you should do it more.

- Be careful – compound interest applies to the debt you owe as well.

So, how will you put compound interest to work for you today?